Welcome to a new era of vendor and employee payments

ACH payments have come a long way. Discover how businesses are using them today.

Employee payroll and expenses. Vendor services and supplies. Business taxes and fees. Years ago, owners would write checks from their business banking account to pay for all these things and more.

As you can imagine, this required a large volume of checks, stationery and stamps as well as countless hours to mail and coordinate everything. Not to mention the fraud risks that can be associated with paper checks.

ACH (short for Automatic Clearing House) Payment Services was created in the 1970s to provide faster, more convenient options, making it possible to transfer funds between bank accounts without paper checks. ACH Payment Services has evolved over the years. And businesses have responded.

Today, more businesses are using ACH payment options to electronically pay business expenses (ACH debits) and accept customer payments (ACH credits). That number continues to grow, with more than 30 billion ACH transactions processed in 2022 alone.

How businesses are using ACH

- To pay employees

- To pay vendors and contractors

- To transfer funds between accounts

- To accept customer payments

Finding more hours in the day

Early on, ACH payments were batched once a day. If you missed the deadline, your payment wouldn’t be submitted for processing until the next business day. On a weekend or holiday, it would take even longer.

This could disrupt a business’s cash flow and delay shipments from vendors waiting for payments to post. As the demand for secure, convenient, digitized payments continued to grow, so did the efficiency with which they could be processed.

In 2016, Nacha, the governing body for ACH payments, added a Same-day ACH delivery option for credits, and it expanded the rules to include debits one year later. 2017 also saw the launch of the Real-Time Payments network that is operated by The Clearing House as a way for merchants to receive their payments even faster.

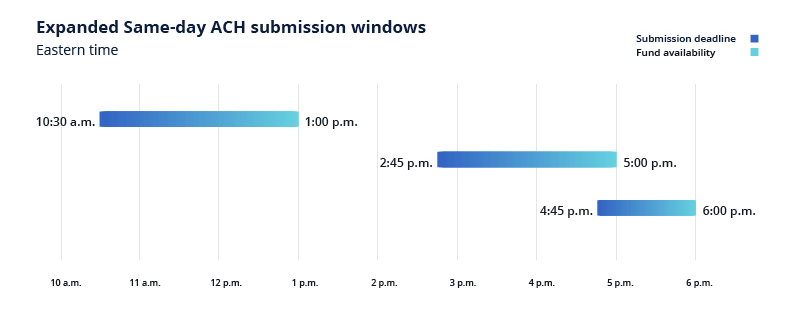

Nacha has continued to improve the service of ACH payments. Submissions are now sent five times a day for Standard ACH and three times a day for Same-day ACH.

Keeping up with changing needs

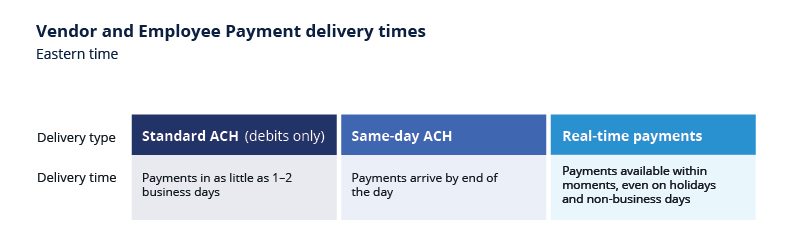

As a business owner, you may sometimes need a payment to post to your account right away. Or you may be able to wait a day or two. That’s where having multiple delivery methods comes into play.

ACH credits can be settled in one of three ways, depending on your needs for that transaction: Standard ACH, Same-day ACH or real-time payment. However, ACH debits (money you pay out) will always post to the receiver’s account by 8:30 a.m. Eastern time the following banking day, or sooner if you use Same-day ACH or real-time payments.

Keep in mind that faster payments may come with additional fees, and not all banks offer Same-day and real-time processing. Chase for Business is one that does. Contact your bank to find out its ACH payment options and associated fees.

Raising transaction limits

In addition to having more submission windows during which to send transactions, businesses can now benefit from higher transaction limits.

This increase helps ensure that recipients get access to larger amounts faster — without having to wait because transactions exceed dollar limits.

Expanding payment options

ACH offers several payment options, depending on your business needs. Most banks charge a flat rate for a set number of transactions per month and an additional fee for any transactions over the limit.

If your number of transactions varies a lot from month to month, you may want to consider a pay-as-you-go option, now offered by some banks. As the name implies, this payment method charges merchants a fee for each transaction — with no monthly flat rate and no limits.

Going digital

ACH payments provide a convenient way to pay compared with paper checks, which can be lost or stolen and may need to be deposited in person. And now, with faster delivery options, new ways to pay and higher limits, these digital payment solutions can give your business even more flexibility and control.

For more information about ACH Payment Services and our pay-as-you-go plan, speak with a Chase Payments Advisor.